As a lender, my goal is 100% transparency with my client. Because of this, I spend a lot of time getting educated on every question a new borrower may have when it comes to closing a loan with us.

One of the biggest pieces of transparency is conveying, as accurately as one can, how much cash a borrower will need to close on a particular loan. While terms differ from lender to lender and even loan to loan, closing costs can be estimated with reasonable accuracy.

The laundry list of fees for a purchase with financing typically looks something like this:

- Owner’s Title Insurance

- Lender’s Title Insurance

- Settlement Fee

- Search & Exam Fee

- Notary Fee

- Commitment Fee

- Deed Prep

- Wire Fee

- Recording Fee

Some of these may vary depending on the state you are in, but this is the gist of it. Now, we just need to estimate the dollar amount for each line item and arrive at the total closing costs.

Again, these fees can vary from title company to title company and state to state. Sounds cumbersome, but that’s why we use closing cost calculators like the one from Empora to do all the heavy lifting.

For the record, it’s worth mentioning that we currently use Empora as our preferred title agency due to their speed of service, investor-friendly services, complete online closing, and overall value. In addition, it’s worth noting that they did not sponsor this post.

So without further adieu, let’s dive into using estimating closing costs with Empora (for free).

Step 1: Click this link to head over to the closing cost calculator: https://www.emporatitle.com/closing-costs-calculator/

Step 2: Scroll down and enter your deal information accordingly.

Step 3: Press “Calculate” and your estimated fees will pop up below.

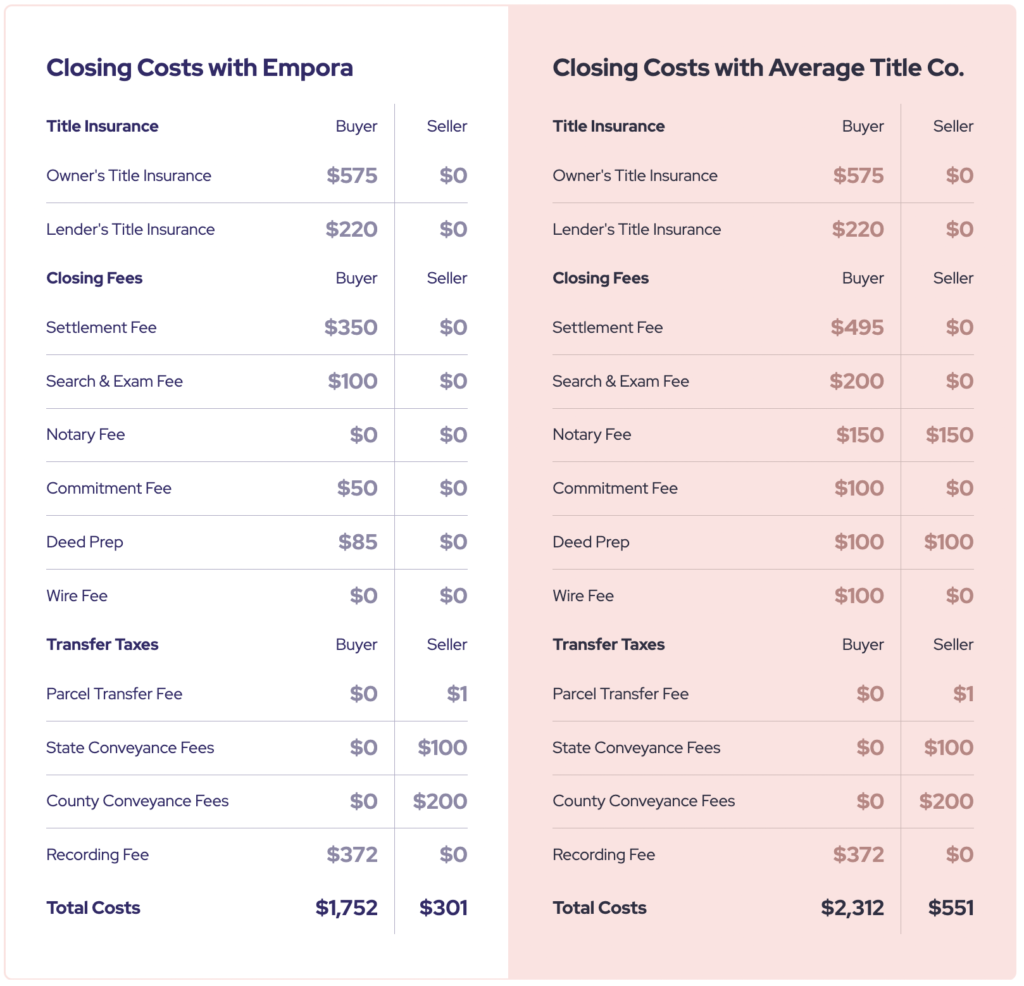

And there you have it. For a property with a $100,000 purchase price and a $75,000 loan in the state of Ohio, the buyer can estimate to pay $1,752 in closing costs to the title company, which in this case is Empora.

At this point, you are probably wondering how accurate these title costs are. As a client who has first-hand experience with Empora, we can attest that these estimates have been highly accurate.

The next question you may be wondering is whether Empora is really that much cheaper than the average title company. In our experience, Empora is consistently one of the lowest-cost title services. However, we personally use them for their investor-friendly team, online capabilities, speed, and transparency.

Remember: Title costs are just a piece of the pie in terms of the total costs of doing your next deal. In large part, your lender will set the stage for how much cash you need to bring to the deal. They will likely require some form of downpayment (0% – 30%+) and have their own list of upfront fees like a loan origination fee, appraisal fee, construction draw fee(s), doc prep fee, and potentially more.

So there you have it. Closing costs made transparent.

The more educated you are about the tools you have available to you as an investor, the better prepared you’ll be to take down deals and scale your portfolio. If you want access to resources including:

- Our 24-hour Project Approval Checklist

- Our guide on How to Analyze a Fix-and-Flip

- Our guide on How to Get No Money Down Financing

- The Pros and Cons of Using Hard Money Lenders

- Access to new releases of the Hard Money Podcast

Then join the Sharper Capital Newsletter for free and get them delivered straight to your inbox.